Gold Price Forecast: XAU/USD is looking for direction around $4,100

- Gold hesitates around $4,100 after bouncing up from Friday's lows near $4,020.

- Investors remain wary of selling US Dollars ahead of the Fed's monetary policy meeting.

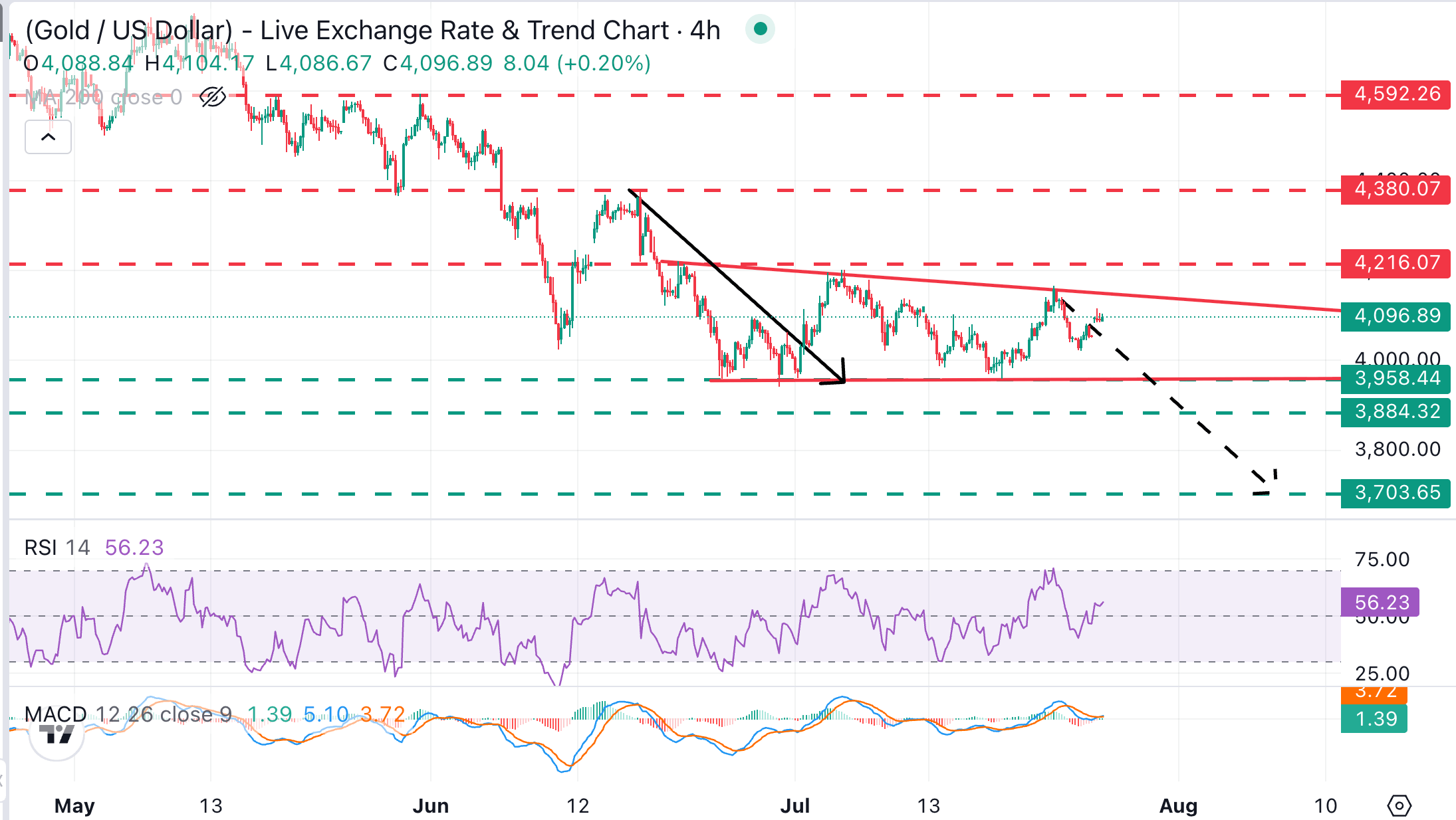

- XAU/USD price action shows a descending triangle in progress.

Gold (XAU/USD) has been consolidating gains during the European trading session, following a bullish gap at the week’s opening as a moderate improvement of risk sentiment hurt the safe-haven USD. A pause in the US-Iran hostilities has boosted hopes of a second round of peace talks, sending Oil prices about $10 lower from last week’s peak and pushing US Treasury yields lower.

Precious metals’ rallies, however, remain subdued so far with investors looking from the sidelines, ahead of the US Federal Reserve’s (Fed) monetary policy meeting, due on Wednesday. Later today, the release of US Durable Goods Orders and the Dallas Fed Manufacturing Index will provide further insight into the momentum of US industrial activity, to frame Wednesday’s decision.

Futures markets are pricing a 33% chance of a Fed rate hike on Wednesday. The most likely scenario, thus, is that of a steady monetary policy, but strong growth data and above-target inflation might prompt the Fed’s Chairman to convey a hawkish message. In this context, the risk is skewed to the downside for gold.

Technical Analysis: Gold is forming a descending triangle

XAU/USD trades at $4,101. The metal holds a constructive immediate bias, yet with price action contained within an ever-narrowing range since late June. Momentum indicators in 4-hour charts are in neutral-to-positive territory, with the Relative Strength Index (RSI) wavering around the 50 midline and the Moving Average Convergence Divergence (MACD) just above zero, hinting at a consolidation rather than an impulsive bullish reversal.

Bulls would need a clear break of the area between the descending trend-line now around $4,160 and the June 22 high around the $4,200 area to confirm a trend shift and bring mid-June highs, at the $4,380 area, into focus.

It's worth mentioning, however, that triangles are often continuation patterns and that, in that sense, a bearish outcome is favoured. Supports are at the triangle's bottom, in the $3,940-$3,960 area, and the late October 2025 low, near $3,885. The Triangle's measured target is at the $3,700 area.

(The technical analysis of this story was written with the help of an AI tool. Know more.)

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.